WASHINGTON, D.C. January 18, 2025 (Reuters) — When Donald Trump pledges in next Monday’s inauguration to “faithfully execute the office of President of the United States”, global economics and politics will take a leap into the unknown. Some of the returning president’s ideas could reawaken inflation just as central banks are taking a victory lap for supposedly taming the last bout of price rises.

The risk is that Federal Reserve Chair Jay Powell and his international counterparts use the same playbook as they have in recent years, with potentially economically damaging consequences. On a different inauguration day, in 1933, former U.S. President Franklin D. Roosevelt declared that the only thing citizens had to fear was “fear itself”. In the case of Trump’s second term, the biggest uncertainty for investors and policymakers is uncertainty itself.

For ratesetters like Powell and European Central Bank President Christine Lagarde, the concern is that inflation could rise if the returning White House resident makes good on his tariff threats. That could send central bankers back to square one just as they are hoisting “mission accomplished” signs to celebrate the apparent end of the last inflationary spiral.

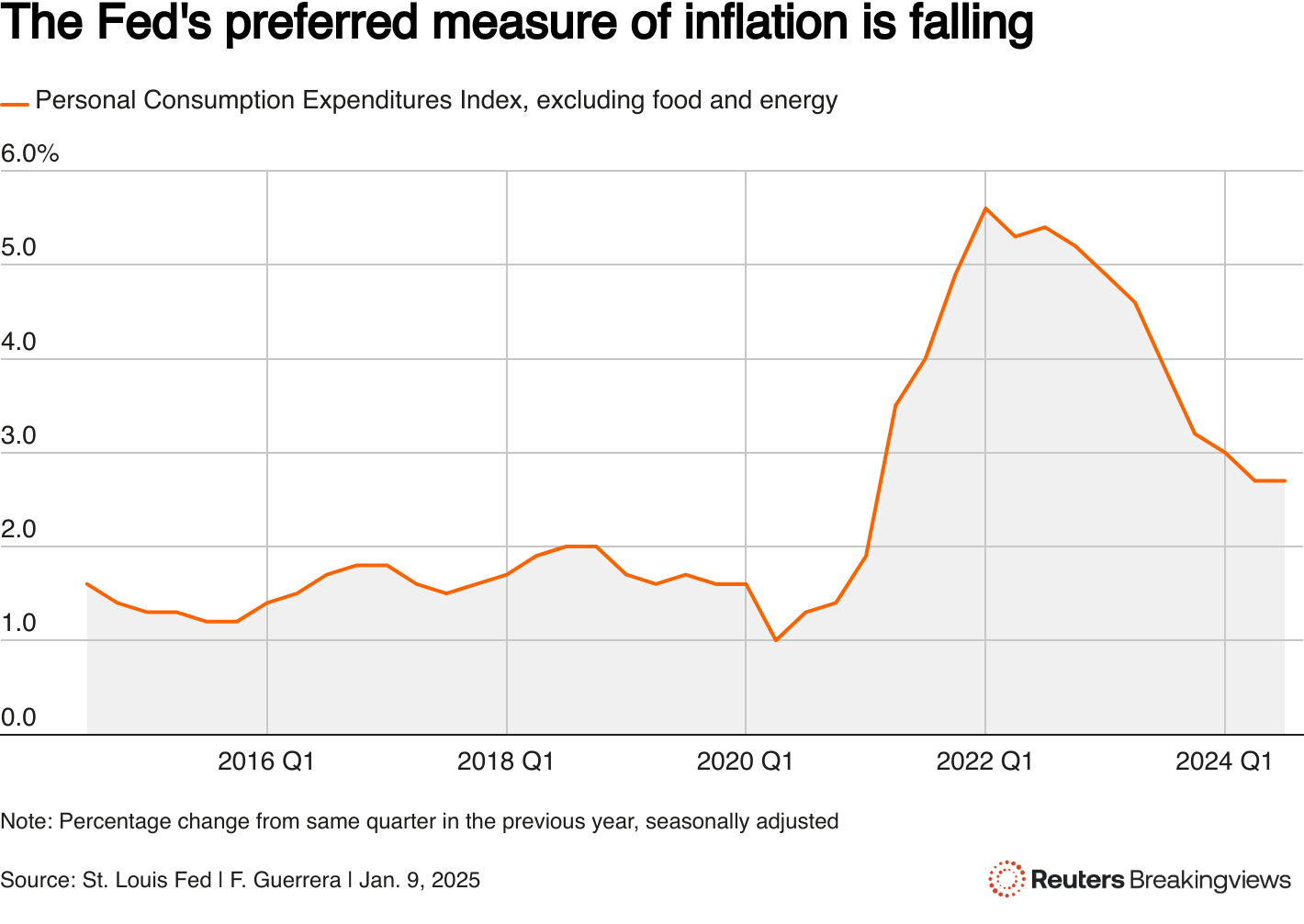

The Fed’s favourite price measure – the core personal consumption expenditures (PCE) index, which excludes volatile energy and food – is growing at an annual rate of 2.8%. Goldman Sachs analysts expect this key inflation metric to hit the Fed’s 2% target in 2025, absent any giant new Trump trade duties.

Yet should the former real-estate tycoon proceed with his floated 100% tariffs on all imported cars and a 60% levy on Chinese-made goods, the core PCE index would end next year at 2.4%, Goldman economist Ronnie Walker estimates. If Trump introduces a blanket 10% tariff on all imports, inflation could soar past 3% again, according to Walker. A consequent trade tit-for-tat would also see prices rise in other economies like China, the euro zone and the United Kingdom.

A new round of global import duties would represent what economists call a “supply shock”. These events are external jolts that make it harder to produce or get hold of goods, putting upward pressure on their prices. Central banks traditionally just waited for these bouts of supply-driven inflation to pass, because monetary policy doesn’t offer a tool to help boost production. A recent study of seven advanced economies by the Bank for International Settlements found that, historically, the monetary response to demand-driven inflation has been three times as large as that for inflation caused by supply shocks.

Yet Powell and his international equivalents jettisoned this softly-softly approach in the face of the recent pandemic supply-chain pressures and Russia-related energy-price surge. Instead of “looking through” the inflation, Powell, Lagarde and Bank of England Governor Andrew Bailey started hunting it with aggressive rate hikes. In a recent speech, BIS Deputy General Manager Andréa Maechler called it “the most globally synchronised cycle of monetary policy tightening in history”.

Did it work? Like a treat, if you listen to policymakers. Researchers at BIS, known as the central banks’ central bank, reckon that inflation today would have been twice the current level if ratesetters hadn’t acted. The implication of this triumphant narrative is that when the next supply shock hits, monetary policy should “lean more forcefully against inflation”, Maechler argued.

Both the analysis and its conclusions have flaws. For a start, inflation’s downfall owes as much to the natural disappearance of supply constraints as to higher interest rates. In a recent study, academics Thomas Ferguson and Servaas Storm found that the Fed’s hikes accounted for between 20% and 40% of the fall in U.S. inflation. In other words, other factors accounted for 60% to 80% of the decline.

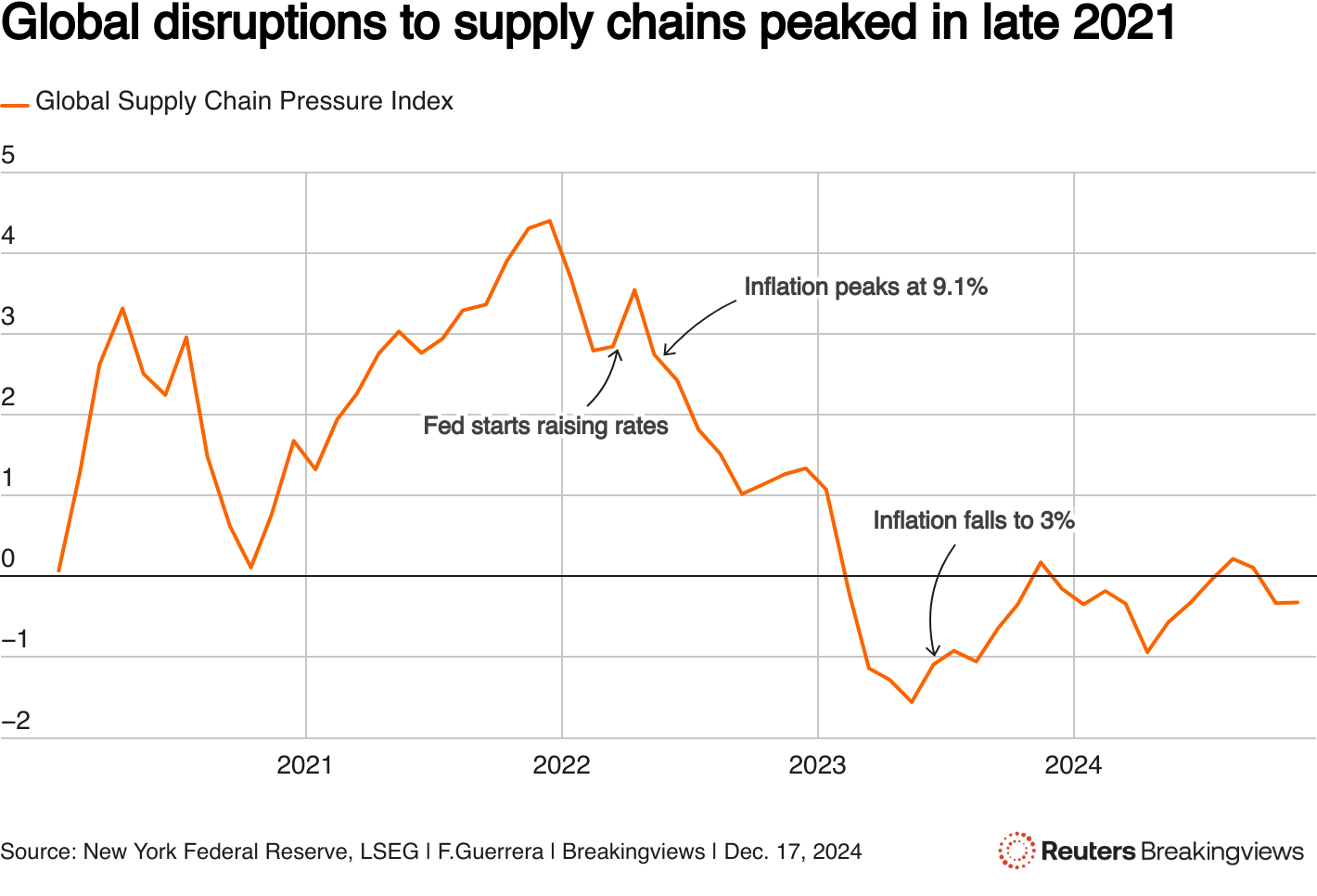

An index of supply-chain pressure compiled by the New York Fed illustrates this point. By the time Powell started raising rates in March 2022, that index was below its record high, but still very elevated. Consumer prices, meanwhile, were rising at a heady annual rate of 8.5%. They peaked at 9.1% in June 2022, but they were back down to 3% a year later. In those months, the Fed did raise rates from around 0% to around 5.3%. But also in that period, supply chain problems plummeted before disappearing entirely in February 2023, according to the New York Fed’s measure.

It is even dicier for central banks to conclude that they could repeat the recent successful “immaculate disinflation”, where rates rose and prices stopped spiralling without a recession. The reasons for this economic miracle are unclear. But they appear to reside in resilient labour markets, driven by European companies’ desire to “hoard” workers for fear of losing them once growth picks up, and an unexpected surge in U.S. immigration and productivity. Those anomalies may not reoccur when the next crisis hits.

This could all be moot if Trump refrains from imposing tariffs or is more lenient than his campaign threats would suggest. But even then, another supply shock, caused by anything from climate change to aging populations or geopolitical strife, may still be around the corner. If they learn the wrong lessons from the most recent war, central bankers may find that “leaning forcefully against inflation” when it’s caused by turmoil in global supply chains does a lot more harm than good.